News

7x24

Quotes

Economic Calendar

Video

Data

- Names

- Latest

- Prev.

Latest Update

Risk Warning on Trading HK Stocks

Despite Hong Kong's robust legal and regulatory framework, its stock market still faces unique risks and challenges, such as currency fluctuations due to the Hong Kong dollar's peg to the US dollar and the impact of mainland China's policy changes and economic conditions on Hong Kong stocks.

HK Stock Trading Fees and Taxation

Trading costs in the Hong Kong stock market include transaction fees, stamp duty, settlement charges, and currency conversion fees for foreign investors. Additionally, taxes may apply based on local regulations.

HK Non-Essential Consumer Goods Industry

The Hong Kong stock market encompasses non-essential consumption sectors like automotive, education, tourism, catering, and apparel. Of the 643 listed companies, 35% are mainland Chinese, making up 65% of the total market capitalization. Thus, it's heavily influenced by the Chinese economy.

HK Real Estate Industry

In recent years, the real estate and construction sector's share in the Hong Kong stock index has notably decreased. Nevertheless, as of 2022, it retains around 10% market share, covering real estate development, construction engineering, investment, and property management.

View All

No data

Light agenda in the next couple of weeks before 2026 begins with a bang.US data to dominate: ISM PMIs, GDP and NFP reports, plus Fed minutes.UK GDP, Tokyo CPI and Eurozone and Australian CPI also on tap.But caution likely ahead of Supreme Court tariff ruling and Trump's Fed pick.

The festive period officially starts next week, with many traders vacating their desks until the first full week of January, making way for thin trading volumes and very few top-tier releases. However, plenty of action is expected in the first full week of January 2026 when the US jobs report returns to its usual schedule.

But what are the risks of volatility episodes such as flash crashes or geopolitical flare-ups during these quiet days when any sudden moves could be amplified due to extremely low liquidity?

With tensions elevated between the US and Venezuela, further escalation is possible. President Trump could decide to take more action over the country by expanding the military strikes on drug traffickers at sea to Venezuelan land – something he's already warned about. The US this week imposed a blockade of all sanctioned oil tankers from entering or leaving Venezuela and Trump could well decide to pile yet more pressure on President Madura.

Fresh tensions would probably boost oil prices and to a lesser extent Gold.

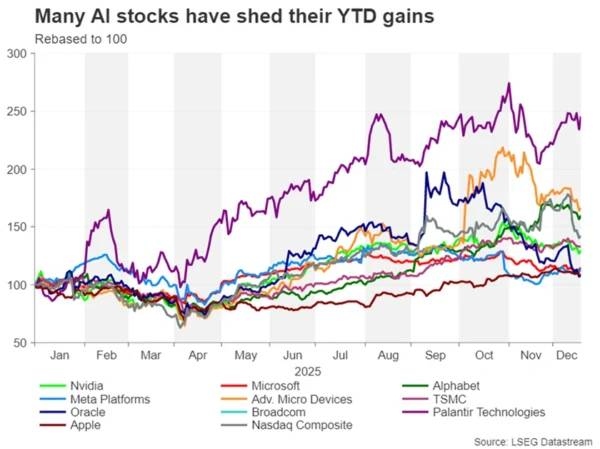

There's also a danger of panic selling on Wall Street if AI jitters persist. Equity markets haven't staged much of a Santa rally this year despite expectations of more Fed rate cuts. But whilst some valuations are clearly overstretched, the AI revolution is only beginning, hence, new winners could enter the scene just as others unexpectedly become losers in the race.

Still, this year's slightly prolonged duration of holiday-thin liquidity increases the risk of a negative AI-related headline triggering a new round of selloff in tech stocks if fresh doubt is cast on valuations.

However, investors on the whole will probably prefer to stay on the sidelines, as they await two key decisions in early January. First, the US Supreme Court will deliver its ruling on Trump's tariffs, ending months of uncertainty about whether most of the levies announced since April are legal or not. However, a ruling against the tariffs may not necessarily be the best outcome, as this could worsen the uncertainty and potentially cost the US government billions if it's forced to refund the tariff revenue to businesses.

The other big decision is who President Trump will nominate to head the Federal Reserve when Jerome Powell's term ends in May 2026. Given that Trump keeps changing his mind and there's a new favourite on a weekly basis, a surprise choice cannot be ruled out. Moreover, picking someone who can achieve consensus within a split FOMC will be crucial. Nevertheless, whoever Trump selects, the new Fed chair will almost certainly be more dovish than Powell, so the announcement is possibly a low-risk event for the markets.

Switching the focus to economic data now, the US agenda is by far the busiest. The advance GDP reading for Q3 is the first highlight next week. Due on Tuesday, the report is expected to show that the US economy grew by a solid annualized rate of 3.2% in the third quarter, somewhat slower than the 3.8% seen in Q2. Durable goods orders for October and the latest consumer confidence index are also out the same day.

On Tuesday, December 30, the Fed will publish the minutes of its December policy meeting. With not a whole lot of Fed speakers out and about during the Christmas and New Year period, the minutes will be scrutinized for any clues on the timing of the next Fed rate cut, as well as to see how strong the inflation concerns still run among the policymakers that voted to keep rates on hold.

Moving into January, things will begin to heat up as the ISM manufacturing PMI for December is out on Monday, January 5, followed by the JOLTS job openings, the ADP employment report and ISM services PMI on Wednesday.

Most important of all, the December jobs report will be released without any delay on Friday, January 9. After the mixed payrolls figures and the much softer-than-expected CPI report for November, any further weakness in the labour market in December would fuel expectations of a January rate cut.

In particular, if the unemployment rate, which hit a four-year high of 4.6% in November, continues to rise, the Fed hawks will find it increasingly tough to defend their stance.

Finally, the University of Michigan's preliminary consumer sentiment survey for December will also get published on Friday.

For the US dollar, the ISM PMIs and NFP data are likely to have the biggest impact. The risks for the greenback are currently tilted to the downside so a bad set of prints could exacerbate any selling pressure.

Employment numbers are also due in Canada on January 9. The Canadian dollar's mini rally versus the greenback paused for breath during the past week after the weak November CPI prints. But an upbeat labour market report could recharge the bulls.

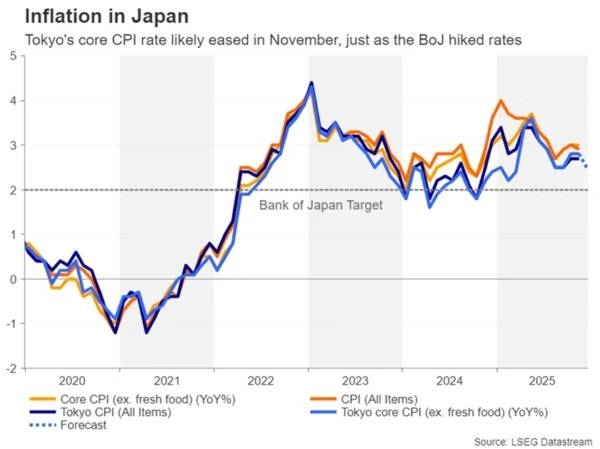

As most traders wind down over the long Christmas weekend, it will be business as usual in Japan. December CPI data for the Tokyo region is out on Friday, December 26, along with the November readings for industrial production, retail sales and unemployment.

Following the Bank of Japan's rate hike in December, the focus is now on how soon the next increase will come. The BoJ will publish the Summary of Opinions of that meeting on Monday, December 29, but before that, any uptick in inflationary pressures could lift BoJ rate hike odds, boosting the yen.

Similarly, investors may want to watch wage growth and household spending numbers that are scheduled for January 8 and 9, respectively.Australian CPI eyed for RBA clues

Elsewhere in Asia, Chinese manufacturing PMIs out on New Year's Eve and January 2 might attract some attention for the Australian dollar. But aussie traders will mainly be keeping their eyes on domestic November CPI data due on Wednesday, January 7.

Although the Reserve Bank of Australia is unlikely to announce any changes in policy at its next meeting in February, any fallback in monthly CPI, which unexpectedly jumped to 3.8% y/y in October, could push back the timing of a potential rate hike, weighing on the aussie.Euro and Pound might shrug off the data

In Europe, it will be extremely quiet apart from Q3 GDP figures out of the UK this Monday, and the Eurozone's flash CPI estimate for December on Wednesday, January 7.

With both the Bank of England and European Central Bank having just held their last policy decisions of the year, neither release is likely to move the euro and pound.

The ECB is firmly on pause at least until the middle of 2026, while any disappointing growth numbers for the UK may not be enough to significantly alter the BoE rate outlook after the Bank delivered a surprise hawkish cut.

Quick Access to 7x24

Quick Access to More Editor-selected Real-time News

Exclusive video for free

FastBull project team is dedicated to create exclusive videos

Real-time Quotes

View more faster market quotes

More comprehensive macro data and economic indicators

Members have access to entire historical data, guests can only view the last 4 years

Member-only Database

Comprehensive forex, commodity, and equity market data